History Repeats Itself in Ad Tech, So What’s Next?

by Lindsay Rowntree on 26th Jul 2017 in News

In association with VertaMedia

Much has been written and debated on the pages of the ad tech industry’s trade publications, websites, and blogs. There is no shortage of opinions, rationalisations, and debates for why things happen, with many points of view, forecasts, and predictions. We have seen many wins and many disappointments. But, writes Chris Karl (pictured below), CEO, VertaMedia, there is no denying that in the real world (the one that happens when you shut down your computer or turn off your phone) history has a tendency of repeating itself.

Guess what? It does in ad tech too! So, as we round the halfway point on 2017, it seems appropriate to look at what has happened over the past few years to determine where things could go in the years ahead. In the immortal words of Yogi Berra: “If you don’t know where you are going, you’ll end up someplace else.” I love that quote.

|

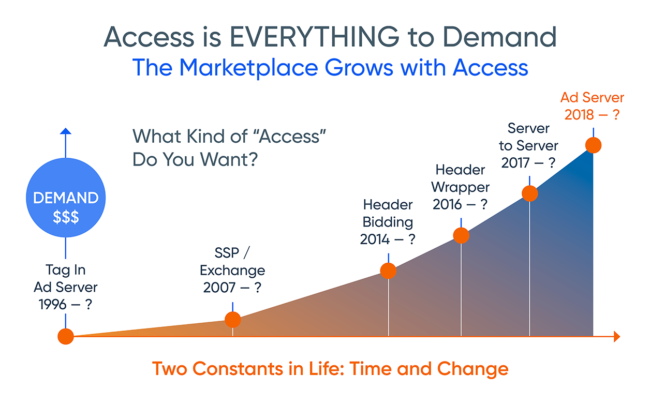

The programmatic marketplace was built for rapid growth, benefitting from the network effect created by robust technology build-outs and experimentation on the buy and sell side of the marketplace. Marketplace growth is enabled by one fundamental premise: ACCESS. In the ad tech market, dollars started flowing from the buy side as more and more inventory became accessible to buyers, first on exchanges then through SSPs. Over the years, there have been many innovations that have enabled access to more inventory. Programmatic access has evolved from a remnant tag in the ad server, to header access, to server-to-server access. History has shown us time and time again that with more access we would see more demand, as the chart below shows.

Source: VertaMedia

As the market has grown, buyers have shown a repeated desire to have direct access to inventory. Whether it be a tag in the ad server, header access, or server-to-server access, buyers will always find their way to the inventory that is performing well for them. History has repeated itself many times over in this area. This makes logical sense because of the gains in technical performance and the economics of the transaction (time and money are important to buyers!). So, while we have been obsessing and debating the merits of header access versus server-to-server access for the last three years, we have ignored the bigger picture: now that buyers have the technical ability to move from back of the line, remnant access to front of the line, premium access (and always want to be direct), we are on the precipice of a huge marketplace optimisation. Why?

Chris Karl, CEO, VertaMedia

Once a marketplace matures, it has a natural tendency to optimise itself. We have already seen this happen on the demand side in several areas. The great agency trading desk experiment has been optimised over the last three years as we have seen the agencies integrate their programmatic experts into their traditional media buying teams – pressure from clients around the margin models for the trading desks and fee transparency certainly helped! One thing happened throughout this process: the DSP/DMP combination solidified its place as the buy-side technology platform of choice and the largest DSPs evolved into SaaS-based businesses (the ones that haven’t have been punished).

Whether you are a direct advertiser, a holding company, or a hybrid (tech plus managed service), you have codified your workflow around the DSP and have consolidated the margin you take on media spend. In this regard, the demand side of the ad-tech marketplace is two or three years ahead of the supply side.

Now what? If history repeats itself, as it has in the areas of demand access and demand process, with the integration of trading desks and the DSP workflow, then we are due for optimisation of the sell-side market around supply access and the sales process. Advertisers, and the pressure they applied to their agencies, initiated this optimisation on the demand side. Who has the ability, power, and control to mandate optimisation on the sell side? The publisher. Publishers with a solid premium brand and decent scale only need to look at history to optimise their opportunity to succeed and thrive in a future when media buying is executed via platforms for all formats and channels.

The future is now and it is inevitable. Firstly, publishers must clearly understand from where their biggest customers’ dollars originate (in their DSP). Secondly, they must understand the various points of access for their customers to buy their inventory (tag, header, server). If publishers decide to go the server route (and use the one everyone uses), they must understand they are accelerating the pace at which they are disintermediated from the buyer. Thirdly, publishers must get as close to that buyer as possible, by integrating directly. Finally, publishers must commit to integrating their direct and programmatic sales and operations organisations, and rewind the clock back to 2006, when they had control of their sales process and knew their buyers.

This approach will create cost savings, increases in CPM, revenue growth, and it will also bring clarity to publishers’ revenue strategy and make their buyers happy. Ultimately, the approach will enable the supply side to catch up with the demand side.

Follow ExchangeWire