Mike Nolet Talks About Dynamic Floors And Second Price Auctions; New US Eco-System Map Is Officially A Mess

by Ciaran O'Kane on 27th Sep 2010 in News

» Mike Nolet, who appeared at the recent Ad Trading Summit, blogs very sparingly these days. But when he does put up a post, it is essential reading for everyone in our space. The topic of his recent post is dynamic floor pricing in RTB, and how it affects the second bid auction. Mike shows some pretty neat graphs from two exchanges using floor pricing. One exchange shows a predictable curve, due to disparity in inventory pricing. The publishers have set lower floor prices for ad impressions, leading to increased demand in the marketplace. The price range is between $0.50 and $2.50. The second exchange featured has an average floor price of $0.90, restricting the number of bids on inventory due to the higher values placed on impressions. The higher floor price has resulted in market inefficiencies in the second exchange. With less demand the price range in this exchange is restricted, and the top price paid for RTB inventory is much lower.

Publishers, as Mike points out, are fearful of cannibalising their top-tier inventory. If brand marketers get a hold of publisher inventory for a fraction of the rate card price through RTB, they would find it extremely difficult to sell it direct at premium prices. The problem here is that DR marketers will not pay those prices. Perhaps something like "blind" RTB would help DR ad traders. In a blind RTB auction, the URL is not shown to the bidder - but bidders will still receive information like context and cookie data. If the exchange only works with premium inventory then buyers will be confident they're not purchasing ads against dodgy content. This means that pubs can set lower floor pricing, and protect top-tier inventory from cannibalisation. Some would say this is a regressive step. But publishers still need to make money to survive - and the premium inventory layer is still the real money-spinner. Where do you think all these impressions come from in the first place?

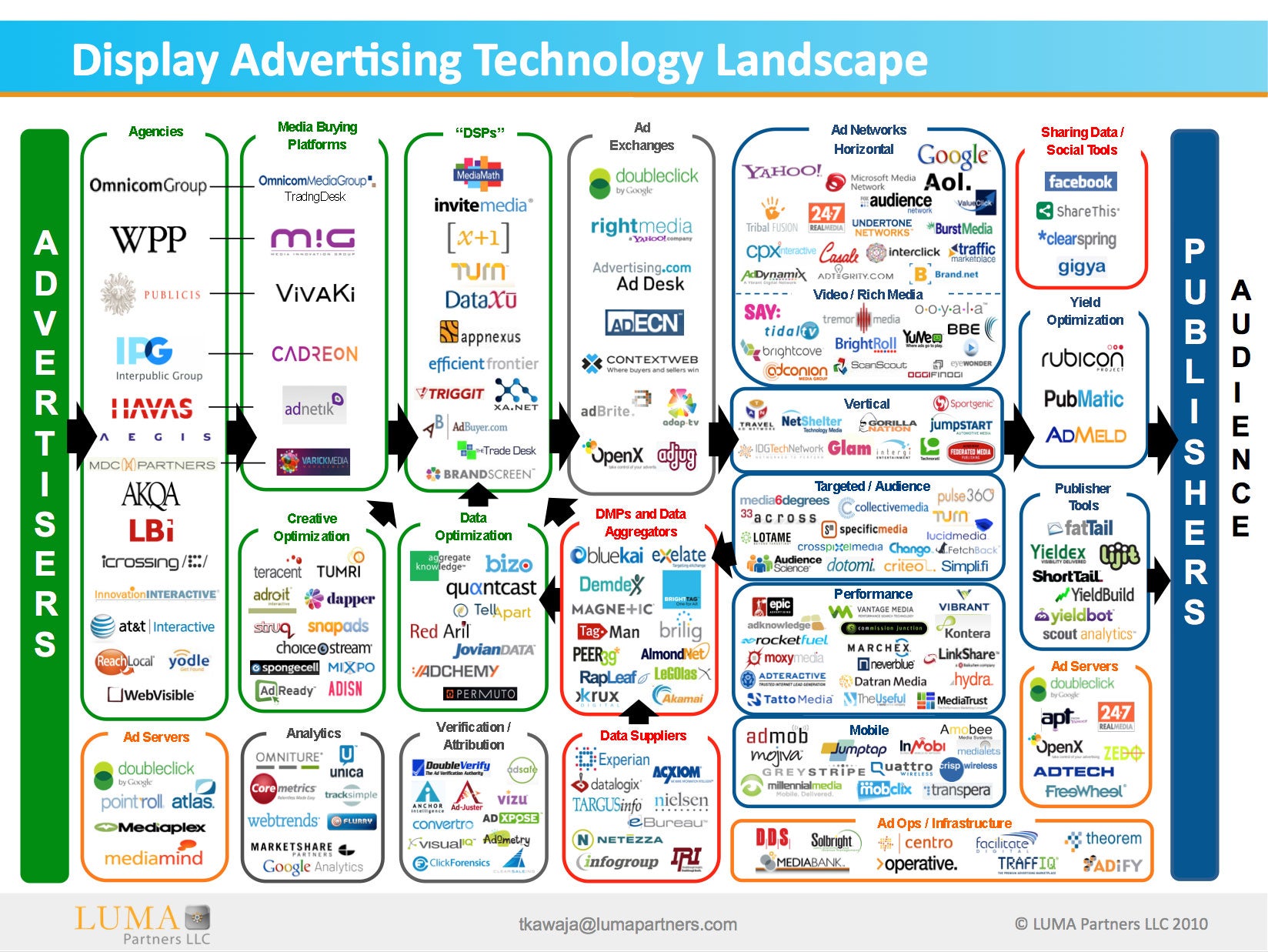

» Terry Kawaja has done an updated map of the US display eco-system - and to put it frankly it is a mess. Between the advertiser and publisher there is an ocean of fragmentation. It's a wonder how anything gets done. I counted about twenty-one layers in total on the new map. How do any of these companies make money? Will they make money? I guess if you're Google, there is little problem. Maybe some of the ad nets - who are now also looking more like DSPs, exchanges and SSPs. I’ve read a couple of tweets this morning saying that disintermediation is inevitable. But I have been hearing that since 2008. And still the map grows. Maybe I'm being too cynical. Perhaps all these companies are making decent coin. Maybe the eight billion dollar display industry can support all these players. But a lot of them would have received considerable VC funding. They can't all be potential multi-million pound businesses. Can they? And can Google/Yahoo/AOL/Microsoft buy everyone? Is commoditisation of the space making the big exit even more difficult? So many questions for a Monday morning.

Ad NetworkDisplayExchangeProgrammaticPublisher

{kind=link}

Follow ExchangeWire