Data-Driven TV Media Buying Solutions: A Brighter Future for Broadcasters, Agencies, and Brands

by Grace Dillon on 16th Nov 2021 in Deep Dive

Identity deprecation. Digitised linear ad breaks. Ever-growing Internet giants. The proliferation of streaming services. A global pandemic. Four trends — and one life-changing experience — that have messily collided over the past eighteen months, bringing advertisers and media owners to the table to resolve decades-long power dynamics by developing win-win solutions, together.

In this Deep Dive, we will walk through the evolution of linear viewership and its downstream effects for marketers who are adapting their mindsets and KPIs to the new, scalable TV formats of tomorrow – Addressable TV (which includes Connected TV). Next, we’ll focus on outlining the broadcaster and technology players in this category, with predictions on the future of these partnerships. Lastly, we sat down with supply-side experts, and long-standing partners of Amobee, Stephen Byrne, Executive Director Europe New Partnerships, and Pieter van den Bergh, Executive Director Europe Demand at smartclip — a pioneer in video advertising technology and services — to discuss their perspectives on this fast-evolving trend and its impact on the industry at large.

Amobee has produced this Deep Dive in partnership with ExchangeWire. Amobee is a wholly-owned subsidiary of Singtel, operating across North America, Europe, Middle East, Asia and Australia. Focused on the unification of TV and Digital, Amobee empowers advertisers and media companies with sophisticated audience-based planning technology that helps them efficiently meet performance goals, while managing the business challenges and technical complexities of the converging world.

The state of the industry today: linear viewership is changing

Years ago, the growing fragmentation across devices drove changes in marketers’ media strategies in planning and buying. Today, however, that change is being driven by the explosion of streaming services, who aptly fight to offer consumers unique access to premium content they can’t live without. More and more, today’s consumers expect to have “TV everywhere”, meaning their willingness to subscribe to a provider is directly correlated to how large and unique the variety of streaming video content is. Atresmedia in Spain is a great example of a broadcaster who has leaned into their own subscription-based on-demand video services (SVOD) and not only delivered exceptional content, but drove increased revenues by monetising audiences’ attention through addressable ad breaks. Within two years of launch, Atresplayer Premium has won National Television awards for Toy Boy and Veneno.

That example illustrates who really benefits from this renaissance of content and the subsequent pricing battles for perpetual monthly revenues — the consumers. Viewers, now more than ever, have better control over the media, channel, and timing of the content they consume (the only holdout being the exclusivity of live sports broadcasts — an outlier to the 24-hour availability of binge-worthy movies and TV shows, and a crown jewel to those who license their live airing rights).

Today, it is evident that the way in which consumers engage with TV content has shifted dramatically, yet it seems marketers’ media plans are just beginning to evolve. Everything considered, Linear TV ads still are the leading medium to communicate with and reach the masses (as Marshall McLuhan termed in 1967), but what has changed is that connected devices and set-top boxes now represent 43%+ of digital video ads viewership — and are growing at a rate of more than 12% YoY. These data points reaffirm that linear TV content will be the next format to shift from direct sales to diversified digital ad revenues.

In addition, a Deloitte study uncovered that amidst a continuing surge in the number of streaming service subscriptions per household, there’s equally a reluctance amongst US TV viewers to spend high amounts on SVOD offerings. This has encouraged many to explore AVOD services, a trend also seen in European markets. Fortunately, this consumer behaviour carves a path for broadcasters and buyers alike to deliver the historic value exchange of free content for advertising ad slots.

The European ATV landscape

Under the umbrella of Advanced TV, or any content delivered beyond traditional linear, the realm of Addressable TV (ATV) is wide and remains ambiguous, as different global markets embrace different terminologies across all players. This generates confusion when advertisers aim to embrace a cross-market strategy, especially when “TV everywhere” is increasingly becoming the new normal. In that way, and as is often the case for nascent technologies, the ATV ecosystem is, in fact, a myriad of ecosystems. Some ATV offerings available in one market are lacking in another, which puts pressure on local and international buyers to become intimately familiar with various offerings that lack a uniform lexicon. To boil it down, ATV is widely regarded as a solution able to align ‘the best of Traditional TV advertising with the best of digital marketing’. Broad as can be.

A report conducted by IAB Europe found that the European market is (unsurprisingly) showing double digit growth on Connected TV inventory — particularly in the EU 5 (the UK, France, Germany, Spain and Italy) — giving broadcasters continuous green lights to double down on digital monetisation strategies.

With vested interests across 67 TV channels, 10 streaming platforms, and 38 radio stations, alongside a robust TV portfolio including Television in Germany, M6 in France and Antena 3 in Spain, the RTL Group is Europe’s largest free-to-air broadcaster conglomerate. The RTL Group’s representative broadcasters have built a blueprint for the industry, both heavily investing in creating their own content, and developing specialised data and targeting offerings for buyers. The foundation of this strategy includes the acquisition of smartclip in 2016. smartclip operates an open ad tech platform tailored to the needs of broadcasters and streaming service providers, facilitating strategic partnerships grounded by cross-media solutions and a uniform tech stack that allows for scalable deployments of monetisation strategies.

Another initiative that has facilitated a standardisation process crucial to the digitisation of TV inventory is the well-known Hybrid Broadcast Broadband TV (HbbTV) mechanism, which has become an industry standard across Europe. As described by the official HbbTV Org, this represents “a global initiative aimed at harmonising the broadcast and broadband delivery of entertainment services to consumers through connected TVs, set-top boxes and multiscreen devices.” In essence, this seamless delivery of TV broadcasts and internet content to the end consumer across their connected devices allows for programmatic ad insertion to the linear ad break — a foundational element to the next wave of addressability on these screens.

The use of HbbTV also helps both TV manufacturers and content providers deploy uniform TV advertising practices across countries. For the consumers, it aligns perfectly with changing media consumption trends, and lets them view different advanced services via one device. Set as a standard in many of the big TV markets, the HbbTV mechanism democratises the addressability of TV advertisements to the wider population and, ultimately, represents a substantial opportunity for ATV advertising, sequential messaging and cross-device targeting.

This technology represents a significant advantage for the European market in contrast to the North American market, where the TV ecosystem affords broadcasters less control over the value chain. This is due to a number of existing MVPDs that offer varying ATV concepts that are underpinned by proprietary technology. So, while the Advanced Television Systems Committee 3.0 technology (ATSC3) could be claimed as the US counterpart to HbbTV, challenging fragmentation still persists.

Irrespective of the technological advancements available today, Europe’s ATV offerings remain dependent on country-specific legal requirements, technical infrastructure, and the direct sale relationships between buyers and sellers of each market. This means that international advertisers can still find it difficult to enter local markets, causing broadcasters to miss out on incremental revenue opportunities.

The advertiser, the broadcaster, and the technology in between

The stakeholders involved in the transaction of ATV advertising all have different needs and diverging interests, which undoubtedly complexifies the standardisation of these capabilities.

On the advertiser side, ATV brings numerous opportunities by providing data-driven inventory. The HbbTV framework, as discussed above, provides a means to digitise TV inventory, which has resulted in an expansion of offers, not to mention advances in content and audience targeting capabilities. Based on who in the supply chain is identifying and collecting signals about the households’ demographics, purchasing behaviours or location, buyers can more feasibly receive a level of access that allows them to deliver a “more targeted” ad.

However, in the wake of identity deprecation, agencies and brands are highly aware that the data flows derived from standardised programmatic ad buying processes (e.g. the bidstream), that currently give them access to the most granular data possible, will no longer function in the future. Thus, their data access for targeting will be nearly entirely reliant on receiving permission from the broadcasters or publishers themselves.

For broadcasters, ATV is driving forward the digitalisation of their traditional TV business, which is under heavy pressure to grow revenues as they watch budgets being shifted to other digital global players. ATV advertising also opens their content up to a wider range of brands and advertisers, whether local or international, who typically lack the resources and/or relationships to advertise on their TV channels. For the marketers, it lowers the entry barriers typically involved in traditional TV buying and offers a new format to their existing workflows, available to all types of advertisers.

Moreover, broadcasters aim to guarantee high standards across delivery, tracking, and measurement to advertisers. This requires broadcasters to invest in technologies that will allow brands and agencies to purchase scalable and state-of-the-art advertising products. There are numerous pressures that remain for broadcasters, including the need to stay competitive whilst the technology evolves, maintaining — and even improving — the level of ad quality in a brand safe environment (which was naturally guaranteed with linear TV), as well as maintaining a good viewing experience.

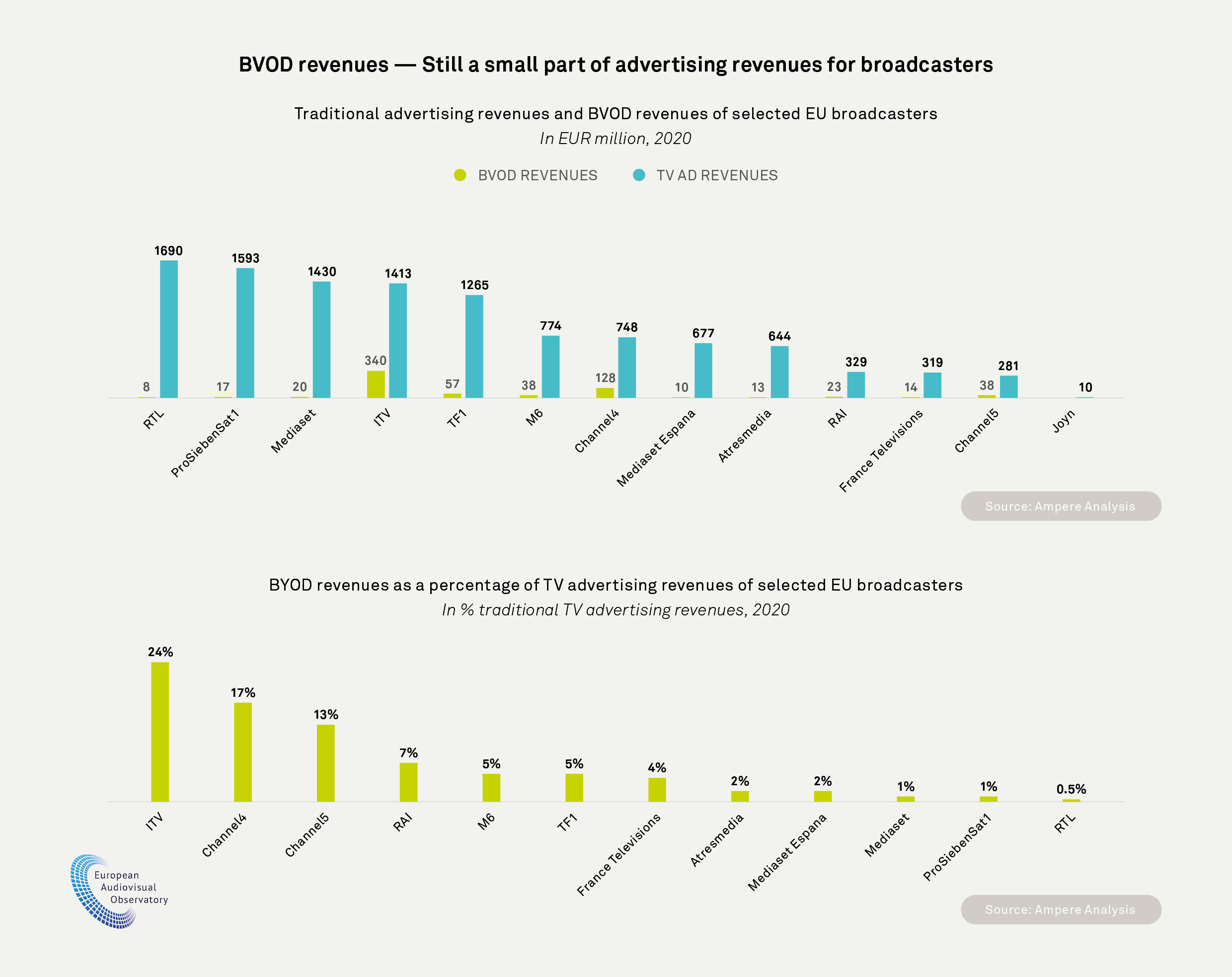

For broadcasters, the win-win solution will be to create outstanding long-form digital content that drives viewership and delivers more impression opportunities to monetise that attention. While they’ve surely done a great job of setting up those ATV monetisation channels, it is now time to develop some data-enabled offerings for advertisers who are more than willing to pay a premium CPM to reach high-value audiences in this environment. Several broadcasters have already started to invest in solutions that give advertisers access to addressable, curated BVOD inventory, offering them full control over buying, tracking, and optimisation processes. One of the pioneers include ITV’s Planet V, which launched in 2020 as an automated buying solution and happens to be underpinned by Amobee’s technology. Their immediate success in the UK has been verified by a study conducted by Ampere Analysis who found that ITV has already generated a significant share of ad revenues (24%) from their BVOD service — reaffirming this strategy can drive substantial growth and revenue opportunities for other broadcasters.

Buyers’ expectations of ATV inventory

European media agencies are now starting to replicate the ATV buying methods of North America — which leads the world in digital ATV advertising spend — and are in pursuit of premium, scalable, and measurable TV content in a handful of places.

From a packaging perspective, broadcasters looking to build ATV offerings for advertisers can deliver better products by understanding buyers’ priorities (which have been highly shaped by their programmatic experiences and expectations). Content and audience targeting, measurement, access to data, and reporting are no longer “nice to have” but rather status quo in all digital media briefs.

On the topic of who is making it “on the media-planning side”, the industry is seeing many TV manufacturers and TV platforms popping up with walled garden offerings – which is to be expected. These companies have dutifully leveraged the diversification of content distribution in their favour, allowing them a bite of the proverbial advertising apple by operating within the supply chain. However, the carriage agreements and seconds or minutes of ad slots can become slim across app owners, MVPDs, TV OEMs and others in between. As such, it’s crucial for marketers to understand who owns the bulk of the bid opportunities (i.e. the content owners themselves) and negotiate more closely with them, rather than leaning on partners who are adding up seconds on each show to build their offering.

Fortunately, digital connected platforms should invariably offer buyers a variety of ways to apply targeting through broadcasters’ ownership of content signals and audience targets, frequency options, reach extension packages, and creative formats.

Ultimately, buyers want direct, transparent and data-driven access to premium publisher inventory — the more premium the better — as it offers the most control on investments. On the other hand, programmatic inventory buying with a cross-channel strategy has also allowed advertisers to reach multiple audiences across multiple content providers through a single platform rather than by directly negotiating agreements with them individually. This way of working is now starting to shift heavily into the ATV inventory space, and will help those buying platforms drive growth by creating synergies between multiple channels and environments.

Unify, standardise and scale

The state of the ATV ecosystem, as it is today, does not come without challenges. With many players coming together, the industry will require ongoing collaboration between the buyers and sellers to help mitigate these barriers and offer secure access to first-party data and unique packaging options.

The varying delivery methods and technical solutions available significantly limit the access to the pool of buying options of ATV ad products. Today, the way to buy ATV inventory heavily relies on direct booking with managed TV platforms, broadcasters, and OTT providers. As the product evolves and grows, advertisers will increasingly require a higher level of data-driven, automated solutions with simplified ad buying access to supply their TV strategies. Similarly, it is to be expected that platforms that are not directly enabling advertisers to access exclusive premium inventory from media owners will eventually become irrelevant in the supply chain.

In addition, one of buyers’ main concerns regarding ATV advertising remains the growth of fraudulent activities within the space. This is why most players are increasingly developing a wide variety of solutions to ensure that audiences are authenticated and viewership is certified. Whilst automated buying to book inventory through efficient processes relies on DSPs and SSPs to facilitate the sharing of first-party data, broadcasters will prioritise having brand safe content and protecting the privacy of their consumers. To do so and deliver on these promises — namely, a brand-safe, privacy compliant CTV space — broadcasters are continuing to develop measurement solutions as the industry evolves. The use of DSPs for CTV advertising will provide advertisers with detailed reporting insights, but some measurement standards — including those for measuring campaign performance, reach and household targeting — still need to be developed.

There is no doubt that there are many possibilities to develop a measurement system in the ATV sphere. Some metrics such as GRPs (Gross Rating Points) or TVRs (Television Ratings) will prevail when measuring audiences with broadcaster or publisher first-party data, but as walled gardens emerge, an agreement across the ecosystem is necessary to counteract and provide advertisers with the ability to measure campaign performance. This is why we expect ATV programmatic ad exchanges to evolve into a shared eco space, where broadcasters can offer exclusive access to premium TV audiences and inventory, at scale across Europe, through secured and approved deals in a unified manner.

Evaluating the state of the European ATV landscape highlights the need to build new and data-enabled TV buying experiences focused on unifying access to inventory across local and international TV markets. As the industry saw with the consolidation of ad networks, whichever organisation brings the principles of simplicity and exclusivity together will win.

What is most exciting about the digitisation of TV is the foundational shifts it can force: like a sudden earthquake, the innovations of the next 12 months have the power to overturn every agency’s “preferred partners” list for years to come.

On the horizon may be such a solution, one that can bring buyers and sellers closer together – where media owners retain sovereignty and independence over their data and inventory assets, while advertisers benefit from a premium programmatic buying experience for long format video inventory. Better yet, a buying experience that doesn’t lock them out of other channels and environments, but delivers synergies to their downstream, omnichannel digital campaigns.

To get an insider’s perspective on the broadcasters’ challenges, choices, and developments, we sat down with long- standing supply partners at smartclip, Stephen Byrne, Executive Director Europe New Partnerships, and Pieter van den Bergh, Executive Director Europe Demand at smartclip.

What challenges do local and international buyers face today in terms of finding scalable, accessible premium inventory in the ATV space?

Pieter: As of today, much of this inventory is being sold through direct bookings to secure delivery. The programmatic inventory availability is rather limited. Broadcasters aim to find a good balance between sharing and protecting data as they understand that data is a valuable part of any offer. Moreover, there is a lot of fragmentation at the moment and there are some discrepancies between broadcasters who all operate differently across the marketplace. In addition to that, ATV is currently only available programmatically in some markets with very specific partners – only through D-Force in Germany, for instance. There is a lack of space to buy ATV programmatic inventory at scale in Europe, and to enable broadcasters to buy next-level programmatic inventory. The aim would be to create one solution that covers it all, including availability for national and international campaigns and exclusive inventory, and where, ideally, all European broadcasters’ inventory would be in one place.

What options do broadcasters have today to monetise their data and content, and what workflow challenges do they face?

Stephen: The main challenge is that broadcasters are using a wide range of technology partnerships themselves, including ad servers, SSP platforms, and selling their inventory to other private marketplaces. The buy-side is often coming in from their own DSP seats, and most of the times these relationships don't match well: one transaction could happen in the Google ecosystem while another does not, requiring them to juggle between several hubs. Due to that, central accountability is significantly lacking, troubleshooting becomes a mess and doing scaled buying is impossible. To solve these challenges, we have already started to create ad alliances, where broadcasters and media owners together can create an alliance of inventory, which can be traded in one place, but often, this still means trading it through several DSPs. Taking it further would include having a fully integrated end-to-end solution.

Pieter: Broadcasters have very unique data, which only exists in the broadcaster ecosystem and is not often shared widely through the whole advertising sphere. There is a need to create a level of confidence and data protection to open up these data points and build great products, which are limited in the market today.

Naturally, broadcasters’ first-party data is heavily safeguarded for now, but what would need to happen for them to feel confident to offer some level of data access to buyers?

Pieter: The necessity lies in having broadcasters feeling comfortable and in control of their data, but also for them to benefit from the data-sharing as well. It is essential to build a legal setup that facilitates these transactions.

Stephen: The option on the table today: broadcasters can choose to work with players who are looking to aggressively create consumer-facing content offerings that ultimately threaten the market share that they have. This is why many broadcasters are not keen to do business with ad tech companies that work with those players.

Moreover, there are some natural tensions between the buy- and sell-side where many scalable solutions are driven from the buy-side perspective. Effectively, they are looking for their own data to be the currency.

There is a chance for broadcasters to get tools that safeguard their own interests and provide a safe space for enabling a data transaction based on their first-party data. In the end, broadcasters’ first- party data is the most premium data that exists because broadcasters have a direct 1-1 relationship with the consumer. I think this is a necessary next step as a supply solution.

What makes broadcaster data so valuable in a post-cookie world?

Stephen: We all know third party-cookies will no longer be the defining identifier in the ecosystem in the next 2–3 years, so the industry is searching for an alternative. Broadcasters are sitting on a treasure trove of data and they have direct access to the household. But some dynamics still need to be managed between operators, distributors, and broadcasters to figure out what the value proposition is. We believe it is incumbent on supply-side players to create an identifier that will enable this premium ecosystem to transact programmatically. We could bring new identity solutions into the mix by allying forces in the future. We still need to remember that different markets have different approaches as well as their own unique measurement bodies in each individual country. The aim is to provide a European solution that is relevant on a national and continental scale.

What would change about buyers’ workflows if there was a unified way to access this inventory?

Pieter: The key priority lies in creating seamless buying experiences that remove all potential hurdles in buying and optimising. From a technical perspective, there is an opportunity to build something that is best-in-class integration wise. In terms of support, buyers usually encounter long, inefficient email threads with support desks from the other side of the world. Hence, there is a strong need for Europe-based support teams who have deep insights into the local market. The ideal scenario would be an addressable product that helps bring the two worlds closer together, through an easy and smooth transaction, by using the data sets and segmentations that are available on both sides. Offering the capability for unified and combined products — both traditional linear TV negotiations and programmatic buying — in the same workflow would be a valuable addition to traditional TV buying.

In a fragmented region like Europe, where does this vision for unified TV inventory buying at scale have the most traction for success?

Stephen: The immediate opportunity for sellers to come together to create a unified video buying front could likely be in some of the smaller markets, where YouTube has given the local media owners a bloody nose when it comes to online video ad spend, but there are various markets where broadcasters want to fight back. These intentions have frequently resulted in alliances. For example, there have been discussions about broadcasters coming together and selling their inventory through Ad Alliance in Germany, Netherlands, and so forth, along with purposeful partnerships like the Premium Video Alliance initiative in Sweden. But of course, the desire is a continental play, even if initial discussions begin on a market-per-market basis. We are fortunate that as a part of RTL Group — Europe’s largest media conglomerate — we are well connected to many internal, but also external, major media companies. And the feedback from all these conversations is overwhelmingly positive (to spearhead a pan-European unified TV inventory buying front) so we already have commitments from major broadcasters to join that initiative. It seems the European media landscape has just been waiting for someone to make the first step in this direction! This is the future that we see in the next 12–18 months.

From a format perspective, CTV, ATV, and online video are the low-hanging fruit. That is, they are already traded today, so they offer immediate opportunity. If broadcasters can bring TV data into the mix and explore linear monetisation more in the future (many broadcasters are moving towards an IP linear model) there are huge opportunities to monetise the digital ad breaks through these methods, and that’s where we will focus our attention next.

Download Report

Download Report

Follow ExchangeWire